Long Live SOFR for Swaps

By Daniel Flaim, Managing Director, North America Interest Rate Derivatives, Tradeweb

It is officially the end of the line for LIBOR. After some 30+ years as “the world’s most important number,” and the last six years on an extended farewell tour, the London Interbank Offered Rate will officially be retired as a benchmark for U.S. dollar swaps transactions. CME Group completed its conversion to the Secured Overnight Financing Rate (SOFR) as the standard benchmark reference for over-the-counter (OTC) derivatives trades in April and LCH will complete its conversion containing U.S. dollar LIBOR vs. fixed interest rate swaps on May 20. By June, roughly $60 trillion in U.S. dollar contracts will be secured to SOFR.

Regulators first announced plans to phase out LIBOR in 2017, ushering in a protracted death march that saw the slow-but-steady migration away from the decades-old benchmark. Ultimately, the Alternative Reference Rates Committee (ARRC) selected SOFR as the overnight benchmark rate to use in certain new U.S. dollar derivatives and financial contracts, and the financial industry—including regulators, central banks, trading venues and other market participants—have spent the last several years getting ready for the transition.

Over the course of that multi-year migration, we’ve learned some important lessons:

Big and complicated problems can be solved when the industry sets its collective mind to something. This transition was no small feat but market participants and regulators quickly rallied together to organize and coordinate efforts ahead of upcoming target deadlines. The end result was a relatively smooth process thanks to solid preparation, decisive action and regular communications.

January 2022 was the moment of reckoning. Migration away from LIBOR was slow and steady before taking a drastic turn ahead of the January 2022 deadline for no new LIBOR origination. By February 2022, SOFR trading on Tradeweb made up 72% of all new risk, and across our business approximately 96% of our most active clients globally trading USD swaps were using SOFR.

This playbook can be utilized elsewhere. We have been pleased to see that the insights and lessons learned from the U.S. dollar LIBOR transition have already extended beyond our markets and into non-LIBOR jurisdictions, further illustrating the permanent impact this movement has had on our global markets.

Why LIBOR Was So Entrenched

Getting there was no small achievement. LIBOR didn’t earn its reputation as “the world’s most important number” for nothing. As the benchmark evolved over the last three decades, it’s been sliced and diced into multiple durations and both backward-looking and forward-looking rates that are used for everything from projecting market expectations for the cost of borrowing to the underlying benchmark for U.S. dollar swaps contracts. Financial technology also grew up around LIBOR, with virtually every piece of financial services software and nearly every financial model incorporating some link to the benchmark.

Thankfully, due to close collaboration between industry stakeholders including trading platforms, dealers and clients, clearinghouses and operators of order management systems, over the course of the transition period, this final step in the migration from LIBOR to SOFR in the swaps market is anticipated to be a smooth one.

Orderly Transition to a New Standard

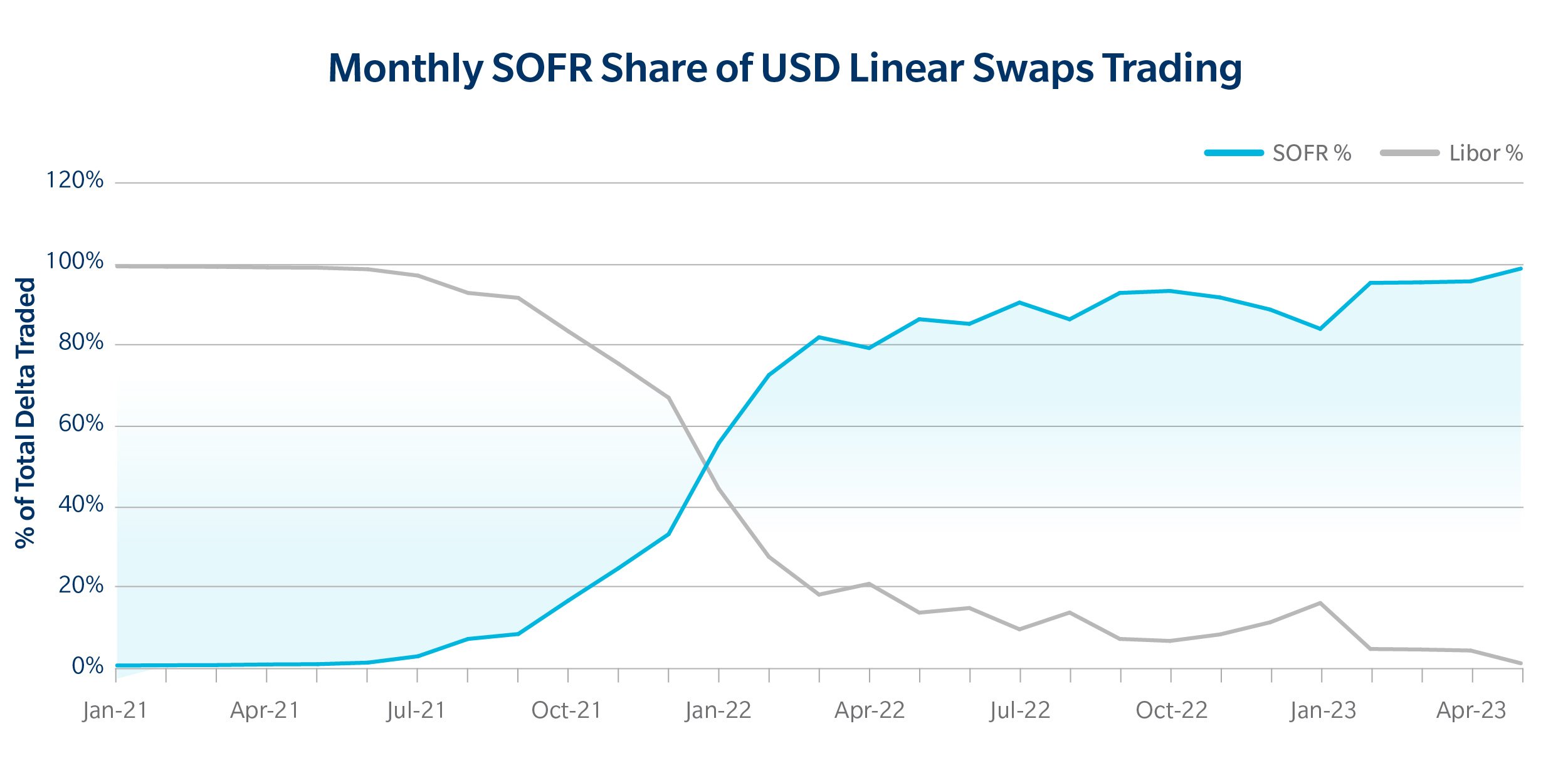

In fact, much of the heavy lifting has already been done. As indicated in the chart below, the percentage of new U.S. dollar swaps trades benchmarked to SOFR and executed on the Tradeweb platform started to trend upward in August of 2021. That date followed the Commodity Futures Trading Commission’s (CFTC) Market Risk Advisory Committee (MRAC) SOFR First recommendation, which introduced a phased approach to the SOFR transition. In the following months, SOFR trading activity on the Tradeweb platform increased as clients began to offset their existing U.S. dollar LIBOR risk, with new SOFR activity reaching parity with LIBOR by January 2022, in response to the upcoming deadline which imposed restrictions on new use of U.S. dollar LIBOR. By February 2022, trading volume benchmarked to SOFR on the Tradeweb platform increased over 50% versus the previous month. In 2022 alone, we had nearly $21 trillion traded in SOFR on the platform.

Source: TW SEF, % of Delta, excluding basis and inflation swaps

Together, the steady forward march toward SOFR adoption for new trades, along with the industry’s diligent efforts to smooth the migration of existing contracts benchmarked to LIBOR, has helped pave the way for an incredibly orderly transition.

Following the success of the LIBOR transition in the U.S. dollar market, we’ve seen similar work being done in non-LIBOR jurisdictions, including Canada. Led by the Canadian Alternative Reference Rate Committee (CARR), Canada is shifting away from the benchmark Canadian Dollar Offered Rate (CDOR) to Canadian Overnight Repo Rate Average (CORRA) as the key Canadian interest rate benchmark. Globally, the LIBOR transition has served as a shining example of industry collaboration overcoming institutional inertia and debunking the myth that things need to be done a certain way just because that’s how they’ve always been done.

Related Content

SOFR First Slowly, Then All at Once: Measuring the Market Transition from LIBOR

The Long Goodbye: Dollar Swaps Markets Bid Farewell to LIBOR