European Credit Update - October 2013

All eyes were on the U.S. in October, mainly thanks to the 16-day government shutdown which saw many key services come to a halt, after the White House and Congressional Republicans failed to reach a deal over stop-gap budget measures needed to keep the government running. A last minute deal on October 16 to fund the government until mid-January and lift the debt ceiling until February 7 was welcomed with sighs of relief across the globe.

Disappointing jobs data released on October 22, combined with concerns about a weaker growth outlook, meant that the Federal Reserve’s decision to maintain its $85bn-a-month bond buying programme announced on October 30 was widely expected. In Europe, Spain emerged from a two-year recession, while Italian PM Enrico Letta succeeded in thwarting Silvio Berlusconi’s attempts to bring down the government.

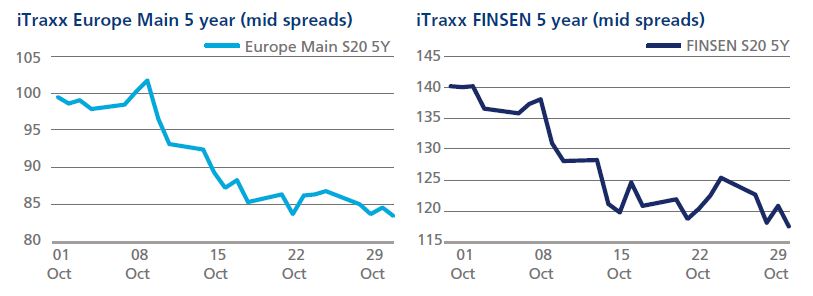

CDS: Spreads on the iTraxx main index have been tightening steadily throughout the month with only a few exceptions - the most notable one occurring between October 3 and October 9, when mid spreads peaked at 101.7 basis points. The subsequent tightening of the index coincided with the first signs of a political resolution in the U.S., reaching 83.4 basis points at month-end.

The Finsen index also tightened considerably during the month by 22.6 basis points, albeit exhibiting higher volatility.

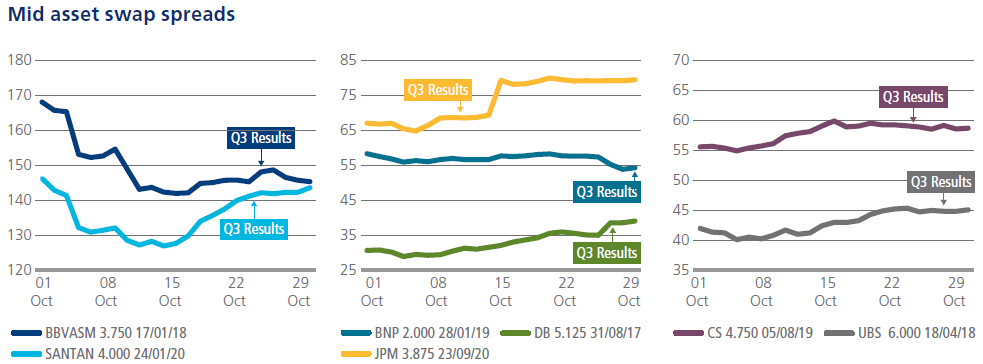

Cash: In the banking sector, October was earnings season with BNP Paribas, BBVA, Banco Santander, Credit Suisse, Deutsche Bank, JPMorgan and UBS - amongst others - reporting their Q3 performance. Results mainly reflected a soft performance in their investment banking division, and weak profits from fixed-income trading.

The European Central Bank also announced that large banks will undergo risk assessments, asset quality reviews and stress tests as early as November, in an effort to restore faith in the financial system. European Credit Data Points

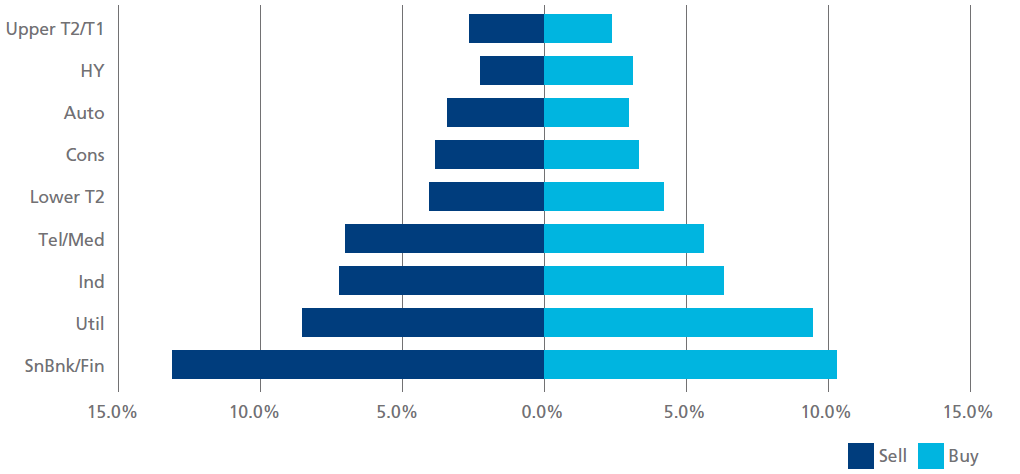

Selling was the dominant trend in October across all European cash credit markets, with the exception of high yield, utilities and the lower T2 banking sector. Senior bank financials is still the most highly traded sector; auto and construction, however, saw a decrease in traded volume from the previous month.