Tradeweb Government Bond Update – August 2025

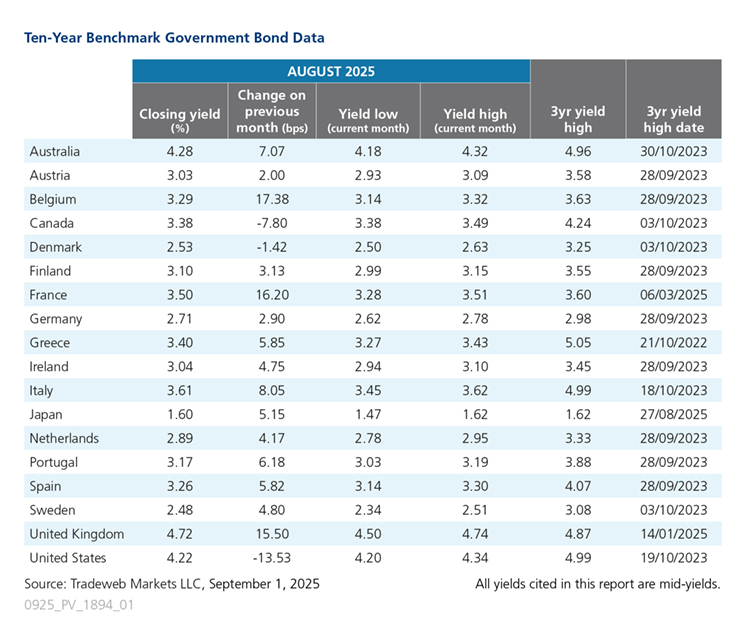

August saw yields in global government debt markets mainly increase, except those for Canada, Denmark and the U.S., where volatility remained a recurring theme. The yield on the U.S. 10-year Treasury fell 14 basis points from July to 4.22% at the end of August.

Bhas Nalabothula, Head of U.S. Institutional Rates at Tradeweb, said: “August brought renewed uncertainty to U.S. markets as economic data drove swings in U.S. Treasury yields across the curve. A weaker July jobs report, with payrolls falling well short of expectations, underscored concerns about slowing labour market momentum. Meanwhile, inflation surprised to the upside, with U.S. PPI rising 0.9% against forecasts of 0.3%. The dovish tones of Jerome Powell’s remarks at the Jackson Hole Symposium on August 22 further fuelled the likelihood of a potential rate cut by the Federal Reserve in September. Against this backdrop, the 10-year Treasury yield climbed to a month-high of 4.34% on August 18, before easing back on softer growth sentiment.”

In Asia Pacific, Japan’s 10-year government bond yield reached a three-year high on August 27 at 1.62%. The yield closed the month five basis points higher than in July at 1.6%. The country’s inflation rate eased to 3.1% in July from 3.3% in June, marking the lowest reading since November 2024, while the S&P Global Japan Manufacturing PMI climbed from 48.9 in July to 49.7 in August.

In Australia, the 10-year benchmark bond yield finished August four basis points up at 4.25%. At its meeting on August 12, the country’s central bank voted to lower interest rates by 25 basis points to 3.6%, citing that “inflation has fallen substantially since the peak in 2022”.

Over in Europe, French Prime Minister François Bayrou called a confidence vote on August 25 for September 8. The yield on France’s 10-year government bond rose to a month-high of 3.51% on August 27, before ending the month 16 basis points higher than in July at 3.5%. In contrast, the country’s inflation rate fell to 0.9% in August, which is below market expectations of holding steady at July’s 1%, according to preliminary estimates.

The yield spread between the French benchmark bond and the German 10-year Bund – a key indicator of fiscal vulnerability, credit risk and overall investor sentiment within the Eurozone – jumped to 81 basis points at month-end. This is the highest level since January this year, and up from 73 basis points at the start of the week and 64 basis points in early August.

Furthermore, the German 10-year Bund yield finished the month at 2.7%, five basis points higher than in July. According to preliminary estimates, Germany’s inflation rate increased to 2.2% in August, up from 2% in July and June, and above market expectations of 2.1%. The HCOB Germany Manufacturing PMI was 49.8, up from 49.1 in July, pointing to an improvement in manufacturing business conditions.

Moving south, Italy’s 10-year benchmark bond yield climbed by eight basis points to 3.61% at the close of August. According to initial estimates, the country’s annual inflation rate inched lower to 1.6% in August from 1.7% in the month prior. Similarly, the manufacturing confidence index in Italy edged down to 87.4 in August, from a 14-month high of 87.8 in July.

Lastly, the UK 10-year Gilt yield increased by almost 16 basis points during the month to 4.72%. The UK’s inflation rate jumped to 3.8% in July, the highest level since January 2024. The S&P Global UK Manufacturing PMI fell to 47 in August from 48 in the previous month. Conversely, the GfK Consumer Confidence Index registered at -17 in the same month, up from -19 in July.

Related Content