From Implementation to Insight: Early Lessons from the UK’s New Transparency Regime – and What Comes Next in the EU

Transparency continues to sit at the centre of regulatory and market structure discussions across European fixed income markets. Following the UK’s move to a recalibrated post-trade transparency regime for bonds and derivatives on 1 December 2025, attention is now turning to how those changes are bedding in and what they may signal ahead of the EU’s own revisions, due to take effect on 2 March 2026.

This article builds on our initial First Look published in December, drawing on two full months of UK data observed on Tradeweb, as well as early February trends and direct feedback from market participants, to outline what firms can expect as the EU framework comes into force next month.

While there are structural differences between the UK and ESMA regimes, the UK observations offer an indicator of how behaviour may evolve under the revised EU deferral rules.

The UK regime: from launch to live market behaviour

The UK’s new post-trade transparency regime marked the most substantive recalibration of reporting requirements since MiFID II/R was introduced in 2018. The Financial Conduct Authority’s objective was to deliver a more proportionate, better-calibrated framework that supports liquidity and resilience across bond and derivatives markets.

A key structural change was the move to a more linear publication model, in which price and volume information is published together, either in real time or following a defined deferral. This replaced the previous combination of size-based thresholds and asset-specific publication conditions, resulting in a more consistent method of post-trade disclosure.

Previously, more than half of UK MTF government bond activity was published via “Next Tuesday IDAF aggregate” (for example: total notional and VWAP across multiple trades, without subsequent trade-level detail). The shift to discrete publication materially improves usability and analytical value of the data.

Under the UK sovereign bond framework, deferral eligibility is determined by issuer, time-to-maturity (TTM), amount outstanding and trade size.

Eligible deferral periods are:

- Real Time

- T+1

- T+2 Weeks

- T+3 Months

For corporate bonds, deferral eligibility is determined by rating (IG/HY), issuance currency, amount outstanding and trade size, with the same four potential deferral buckets.

What we are seeing so far

With the revised UK regime now live since 1 December 2025, we have two full months of post-implementation data (December and January), plus early February observations based on Tradeweb’s own internal view on eligible deferrals applied. The impact has been both immediate and measurable, though evolving.

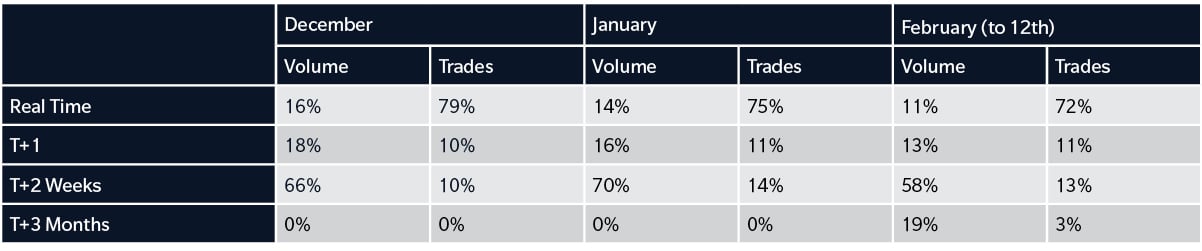

- Sovereign Bonds (Tradeweb UK MTF – EUR notional)

Pre-change (November proxy)

Extended deferral was effectively the default outcome:

Only 3% of EUR notional volume was published in real time, while 56% was published via indefinite aggregation.

December to mid-Feb (post-change)

The sovereign market shows a classic regulatory response curve: initial transparency expansion followed by threshold optimisation.

In December, real-time publication increased more than fivefold (3% → 16%), with a further 18% of volume visible within one trading day via T+1. No trades qualified for T+3 Months in December or January.

By early February, however, the first material use of the T+3 Month bucket emerged, accounting for 19% of venue volume and 18% of UK APA volume. Real-time proportions have moderated from their immediate post-implementation peak, with activity redistributing toward longer deferral buckets.

While still early, this pattern suggests participants are increasingly calibrating trade size and execution strategy to access longer deferral protection under the revised thresholds.

The full impact, particularly for trades qualifying for extended buckets, will become clearer as longer deferral cycles complete.

For reference, sovereign bond qualification thresholds are:

T+2 Weeks

- TTM < 5Y: £50mm+

- 5Y < TTM < 15Y: £25mm+

- TTM > 15Y: £10mm+

T+3 Months

- TTM < 5Y: £500mm+

- 5Y < TTM < 15Y: £250mm+

- TTM > 15Y: £100mm+

The full impact of the regime, particularly in relation to longer-dated deferrals, will become clearer once trades qualifying for extended buckets have completed their publication cycle.

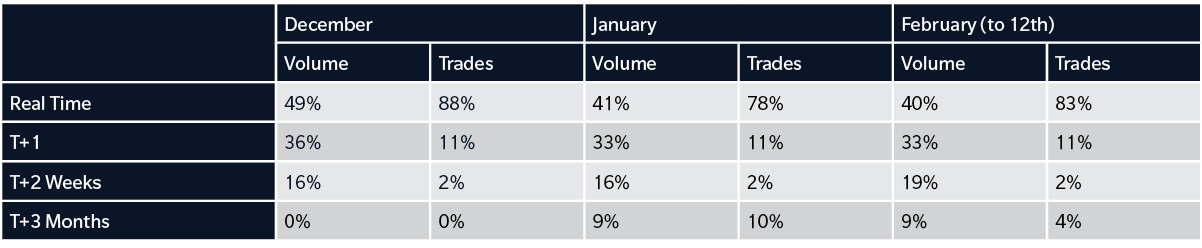

- Corporate Bonds (Tradeweb UK MTF – EUR notional)

The reset in corporate bond transparency has been even more pronounced.

Pre-change (November proxy)

Nearly every corporate bond trade prior to December had the longest eligible deferral applied.

December to mid-Feb (post-change)

December marked a structural inversion. Real-time publication moved from effectively 0% to 49%, and 85% of EUR notional credit (Real Time + T+1) became visible within one trading day. The longest deferral bucket, previously capturing 95% of volume, fell to 16%.

Through January and February, immediate transparency has remained structurally higher than under the prior regime (74% and 73% respectively within one day), with real-time stabilising around 40%. At the same time, T+2 Week and T+3 Month deferrals have begun to feature more consistently, indicating emerging behavioural calibration.

What market participants are saying

In recent weeks, Tradeweb has hosted client roundtables focused on transparency reform and data consumption.

Across these discussions, several consistent themes have emerged, including unsurprisingly that the value of post-trade data depends not just on availability, but on how effectively it can be interpreted and incorporated into trading and investment workflows.

Many market participants signal a preference for aggregated, contextual views of activity, such as traded volumes over defined time periods or directional indicators, rather than relying solely on individual trade prints. As real-time and T+1 volumes increase (for example, 85% of UK corporate bond volume in December and 73–74% in January/February now visible within one day), the opportunity to build such contextual analytics becomes more immediate.

There is also growing interest in integrating transparency insights directly into execution workflows, allowing recent activity and liquidity conditions to be assessed at the point of decision-making. This theme is becoming increasingly relevant as discussions around the go-live of the respective UK and EU Consolidated Tapes approaches.

In the EU in particular, the sequencing of reforms is shaping discussions. With revised transparency requirements taking effect at least 9 months ahead of the introduction of a public consolidated tape, market participants are considering interim approaches to aggregation and analysis to bridge that gap.

At the same time, increased transparency is sharpening focus on data quality and consistency. As publication volumes rise, participants are paying closer attention to issues such as duplicated prints, misreported sizes and the classification of more complex trading activity.

Preparing for the EU’s transparency changes on 2 March

While the UK framework has transitioned to a simpler, linear model with discrete publication and defined deferral buckets, the EU’s revised post-trade transparency regime will retain a more granular and multi-layered structure when it comes into effect on 2 March 2026 (with supplementary deferrals for a subset of sovereign bonds applying on 4 May 2026).

The changes will apply to bonds, exchange-traded commodities and structured finance products, with derivatives expected to follow next year. Under the EU framework, price and volume may be published at different points in time, and a wider range of conditions will determine eligibility for real-time publication. Deferrals will follow a more segmented sequence depending on instrument type and size.

As a result, transparency data in the UK and EU will increasingly follow distinct publication patterns, even where underlying instruments and participants overlap.

Although calibration differs, the UK experience demonstrates that changes to deferral thresholds can materially and immediately alter publication profiles including a rapid increase in real-time visibility; a compression of activity into T+1 as well as subsequent behavioural adjustment toward longer buckets once firms assess qualification thresholds.

These directional signals may provide a reference point as ESMA’s revised framework comes into operation.

Implications for cross-border transparency consumption

The coexistence of two calibrated but structurally different regimes is prompting firms to reassess how they consume post-trade data at a European level.

One area of focus is potential dual reporting in cross-border scenarios, where the same financial instrument may be subject to different publication rules depending on venue, counterparty and execution method. Divergent publication timing, particularly as longer deferral buckets begin to see use, increases the complexity of aggregation and comparison across regions.

Data reliability and enforcement are therefore gaining prominence, particularly in segments where off-venue trading remains significant. Venue-reported data is often viewed as more consistent and predictable, reinforcing its role as a reference point for transparency analysis.

Looking ahead

Two months into the UK’s recalibrated regime, the direction of travel is clear: transparency has increased materially, extended deferral is no longer the default outcome, and behavioural adjustment is beginning to emerge as firms engage with the new thresholds.

Tradeweb will continue to monitor publication trends across both jurisdictions and engage directly with market participants. Further updates will follow as EU data becomes available and cross-border patterns begin to emerge.

If you would like to explore the new UK post-trade transparency regime in more detail, you can visit our real-time MiFID publication site, where prints from our UK MTF and APA are available here - select “Contact us for real-time access” if you need login details. For additional guidance on using MiFID post-trade data, your Tradeweb relationship manager can share those resources with you.

Related Content

First Look: Week 1 of the UK’s New Transparency Regime Calibration