From SEFs to Repo Clearing: Industry Lessons for Streamlining Adoption

Elisabeth Kirby

Managing Director and Head of Market Structure, Tradeweb

This article originally appeared in Finadium here.

A series of seismic changes to the underlying market structure of US Treasuries markets will radically reshape the way fixed income markets operate.

New rules, introduced late last year by the Securities and Exchange Commission (SEC), require that the majority of Treasury trades will soon need to be cleared through a central counterparty clearinghouse. Phased-in starting in March of 2025, with Treasury cash clearing beginning December 31, 2025, and repo clearing beginning June 30, 2026, the clearing mandate has raised many questions among market participants about how, exactly, the clearing process will work and whether or not it will introduce new risks, increase capital requirements, and create trading inefficiencies.

These concerns are particularly acute in the $8.13 trillion repo market, where the introduction of a central counterparty could create some unique challenges. Chief among those is the fear that the ability to cost-effectively deploy capital using Treasury holdings as collateral could be strained once a third-party is introduced into the trading workflow.

For those who’ve been around long enough to remember, the new clearing mandate, and the marketplace’s concerns about implementing it, are reminiscent of the derivatives markets reforms introduced as part of Dodd-Frank following the financial crisis. Conceived as a way to increase transparency and remove counterparty risk, central clearing of derivatives also raised serious concerns for market participants who believed mandated central clearing would sap liquidity, cause a buildup of risk at the clearinghouses, and increase trading costs.

Those worst-case scenarios were not realized, however. Thanks largely to innovation on the part of trading platforms and derivatives market participants, the transition to centrally cleared derivatives trading went smoothly, ultimately driving a significant increase in electronic derivatives trading volumes in the years that followed. One of the key players in that transition was Tradeweb, which developed an electronic pre-trade credit check solution that allowed both parties to the trade and the clearinghouse to assure “certainty of clearing” before the trade was even executed.

Now, Tradeweb says the lessons learned developing their pre-trade credit check protocol for derivatives are proving relevant for repo markets as they confront these new changes.

Preparing for Repo Clearing

To fully understand how these lessons can be applied, it’s important to first understand the scope of the changes that will occur in repo markets.

Looking to June 2026 when the repo clearing mandate goes into effect, market participants are starting to prepare for repo trading and clearing from operational, credit and legal perspectives. DTCC’s July 2024 Industry Pulse Check showed that “many firms are continuing to digest the impact of the SEC Treasury Clearing Mandate on their businesses and working to crystalize their strategies and business plans.” Working with an experienced trading platform to ensure readiness offers a reliable path for all types of counterparties to successfully go live.

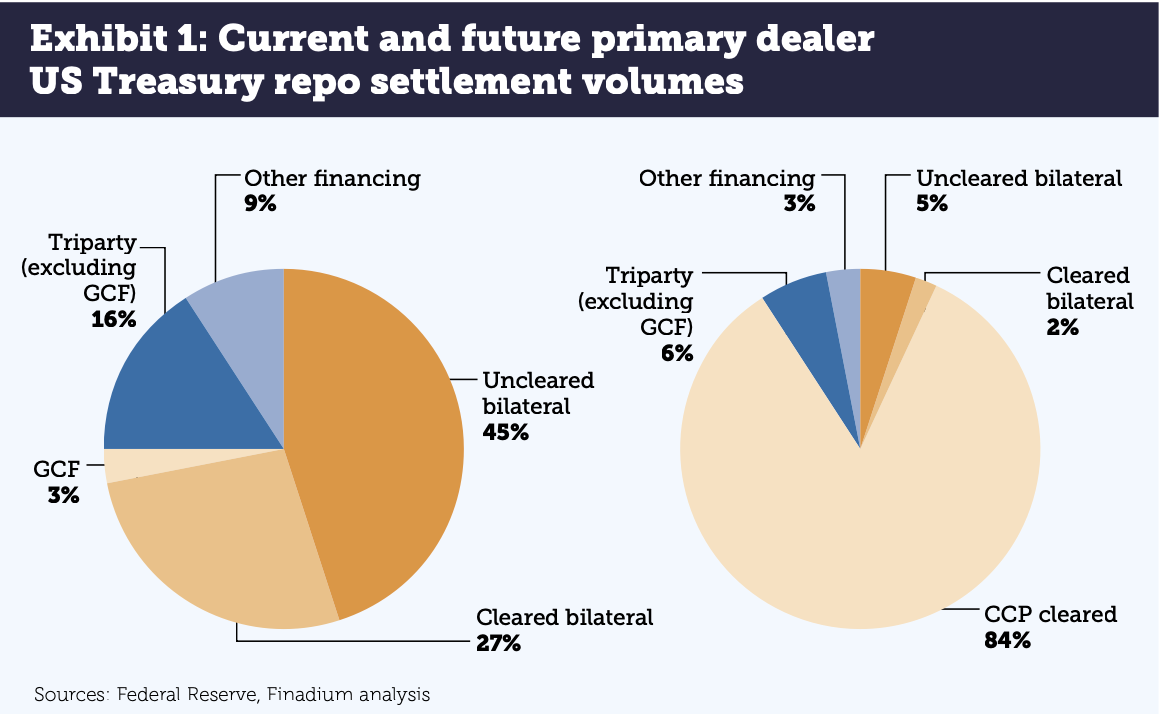

The amounts expected to move to repo clearing are large; DTCC says that it expects daily Treasury Clearing activity to increase by more than $4 trillion. US repo primary dealer statistics show that uncleared US Treasury repo is currently 70% of the business. After the mandate goes live, CCP cleared business is expected to reach 84%, according to Finadium analysis (see Exhibit 1). While market dynamics will shift in the short term, comparing the SEC’s rules to available data show the magnitude of change ahead.

The size and complexity of the repo market, combined with its short-term nature, present unique challenges. With trillions traded each day, usually over a period of just a few hours and as part of much larger portfolio trades, the repo market thrives on relationships, trust and ultra-low latency. The introduction of a third-party into that equation runs the risk of slowing things down, creating a build-up of risk in the clearinghouse, and – potentially – requiring firms to put up huge amounts of collateral to back those trades.

Currently, the specifics of the individual clearing models that will be used for repo trades are still in flux. The Fixed Income Clearing Corporation (FICC), which currently handles the majority of US Treasury clearing, supports a sponsored access model, whereby members bundle clearing and execution with the sponsoring bank or dealer in what is called a “done with” trade. However, FICC is also reportedly exploring an alternative model, which is based on an agency clearing model, whereby buy-side firms trade with an executing broker who underwrites the client’s exposure to the clearinghouse, similar to the models proposed by CME Group and ICE. This approach, which is widely used in derivatives markets, is commonly referred to as “done away” trading. Other clearing houses, and their associated models, may still emerge.

Whichever model the clearinghouses land on, many market participants have already started to sound alarm bells that the process could introduce unintended consequences.

The Importance of Credit Checks

As these concerns continue to mount, the derivatives reform analogy becomes even more appropriate. An important element of OTC derivatives clearing is ensuring “certainty of clearing.” To help that process along, in 2013, just as OTC derivatives clearing was about to be mandated, Tradeweb developed an electronic pre-trade credit check functionality, which acted as a sounding board to ensure swaps transactions had all the right ingredients to clear seamlessly. This pre-trade credit check is now market standard in electronic OTC derivatives trading.

The process works by creating a mechanism whereby both parties to the trade and the clearinghouse can assure that the trade will clear through a futures commission merchant (FCM) before a swaps trade is initiated. This pre-trade credit-check procedure can occur at the clearinghouse, through an industry vendor or hub, or at a trading venue called a swap execution facility (SEF), where the trades are actually executed.

The credit check process requires that a trusted intermediary holds information that both parties can use to validate that a trade will clear. Ultimately, that additional step, built directly into the electronic trading workflow, delivers the necessary transparency and checks-and-balances needed to process the trade without an unnecessary build-up of collateral.

A similar model is likely to be necessary for repo, where many participants are expecting a done away model to emerge. A credit check requirement means that firms will likely need to utilize a trading platform or vendor offering this service for electronic and voice trades alike. Our conversations with market participants show that most if not all want pre-trade credit checks in repo clearing. This will enable every firm to have the certainty that they can trade with any other counterparty at any time.

The Swaps Clearing Experience: What We Learned

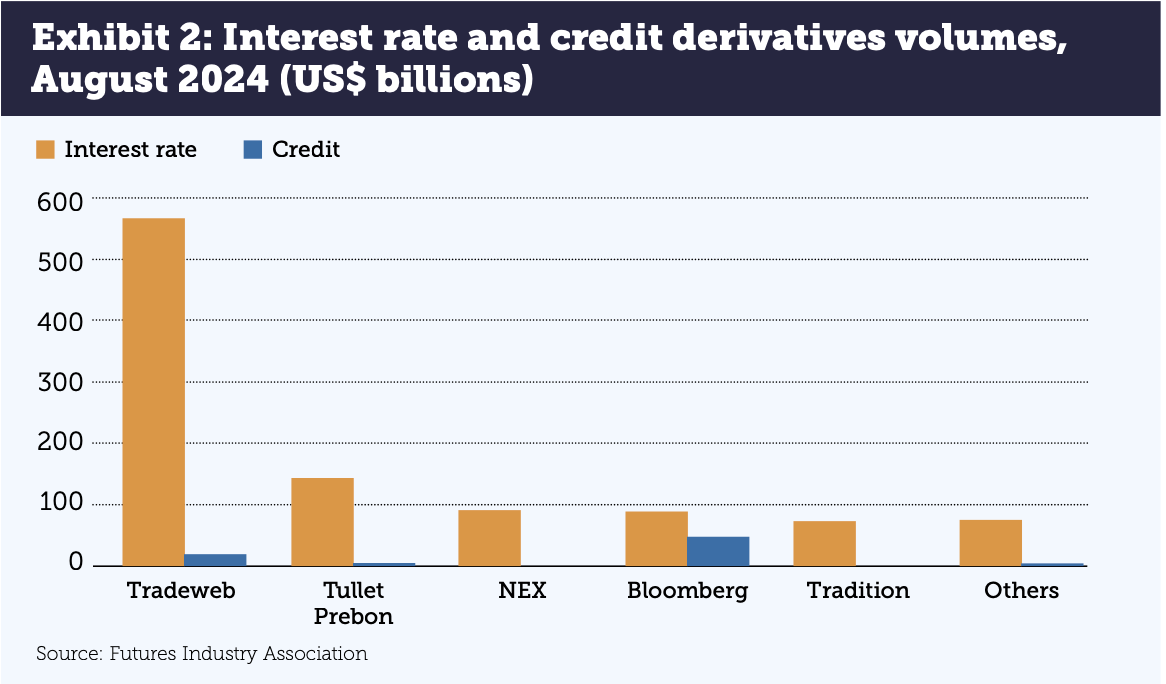

The CFTC introduced a swaps clearing mandate in 2014. Swap execution facilities (SEFs), which came into existence the year prior to the clearing mandate, have facilitated the majority of such centrally cleared swap trades. There have been 33 registered SEFs launched since mandatory clearing was introduced in the derivatives markets, but the majority of business today is conducted on a handful of platforms: in interest rate derivatives, Tradeweb has a 55% market share according to the Futures Industry Association (FIA) (see Exhibit 2). When looking only at Dealer to Client (D2C) trading, this share becomes even greater. In D2C trading, end clients have utilized SEFs to achieve greater trading efficiency while staying compliant with regulatory mandates.

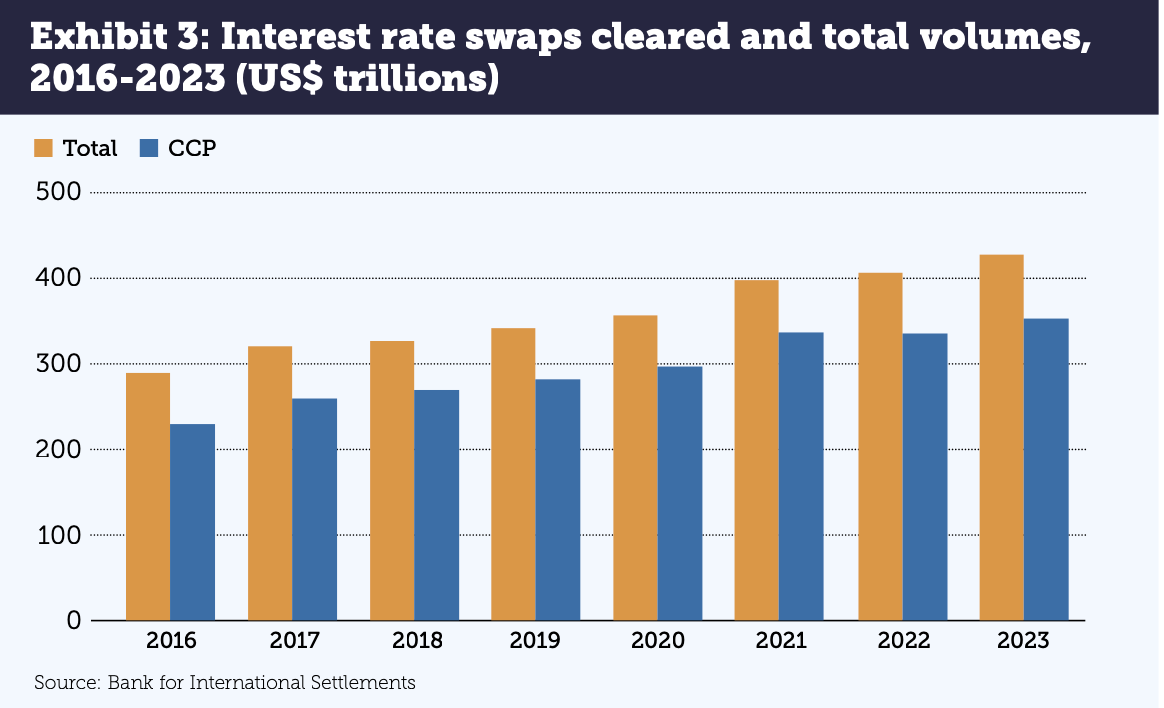

The CFTC and similar swaps clearing mandates around the world have been successful: Bank for International Settlement data show the market share for CCP-cleared interest rate swaps has ranged from 80-85% from 2016 through 2023 along with steadily growing total volumes (see Exhibit 3). SEFs that capture electronic transactions, send it to central counterparties (CCPs) for clearing and assist in reporting obligations have become the industry standard.

Applying SEF Lessons to Repo Clearing

The emergence of SEFs, market consolidation and the need for specific functionality in the OTC derivatives market all have immediate lessons for repo clearing models. Tradeweb experience in the SEF market has four direct impacts for repo today.

- Portable technology from other markets can reduce cost and time to market. Tradeweb’s market leading SEF technology can be leveraged to support repo clearing.

- Tradeweb support in strategy and market intelligence can be critical to success. Market participants are faced with several decision factors in their move to central clearing. Dealers and clients will have to sort through not only trading platforms but also the exposure and balance sheet impact associated with various clearing options. As a central trading venue with connectivity to the majority of large market participants, Tradeweb can help clients understand the implications of the various options on the table and establish connectivity that works best for them.

- Many vendor platforms today may reduce to a few liquidity centers within three years. There are at least eight repo trading platforms today and more may launch to capture new business from the repo clearing mandate. However, the SEF experience showed that a dispersion of market liquidity at first can fade away later, with two or three market centers capturing the majority of business. It would not be surprising to see the same thing happen in US Treasury repo.

- Credit checks in repo are likely to become a needed functionality. Already, market participants are asking for the pre-trade credit checks they use in the swaps market to be available in repo clearing as well. Market participants should validate that any platforms and vendors they plan to use can offer this functionality early in the process.

As best practice, we recommend that market participants assess their own experience in the OTC derivatives market for next steps in repo clearing. What worked best? What did firms think was going to work but didn’t? How did market structure change after the first burst of energy in the initial years? Many of the same types of transitions are likely to occur in repo. Firms that evaluate their own history and learn from platforms that have been through a similar regulatory cycle are likely to benefit going forward.

Related Content

Repo Market Needs Clearing Certainty

SEC Treasury Clearing Mandate: What Market Participants Need to Know