First Look: Week 1 of the UK’s New Transparency Regime Calibration

Transparency is once again becoming a hot topic of conversation across European financial markets. The first major milestone occurred in the UK, where a new post-trade transparency regime for bonds and derivatives went live on December 1, 2025.

The launch marked the most substantive adjustment to transparency requirements since the original implementation of MiFID II/R in 2018.

In its policy statement PS24/14, the UK’s Financial Conduct Authority (FCA) stated that the outcome it sought was a more “proportionate and better calibrated transparency for bond and derivative markets, with requirements tailored to different asset classes and market structures” that “support market liquidity” and “contribute to a more resilient system that enables well-functioning markets in both normal and stress market conditions”.

So, what has changed? One of the main revisions was to expand the conditions under which price and volume information is published in real time for bonds and standardised over-the-counter (OTC) derivatives that qualify under the post-trade transparency rules. This includes bonds traded on a UK trading venue and certain derivatives that fall within the scope of the derivatives trading obligation or the clearing obligation.

The UK’s new linear approach replaces a previously fragmented structure in which real-time publication was mandated where applicable, and deferred publication followed one of several defined “large-in-scale” or cap thresholds. Under the current framework, price and volume appear simultaneously at the point of publication, creating a uniform method of release for post-trade information irrespective of the applicable deferral.

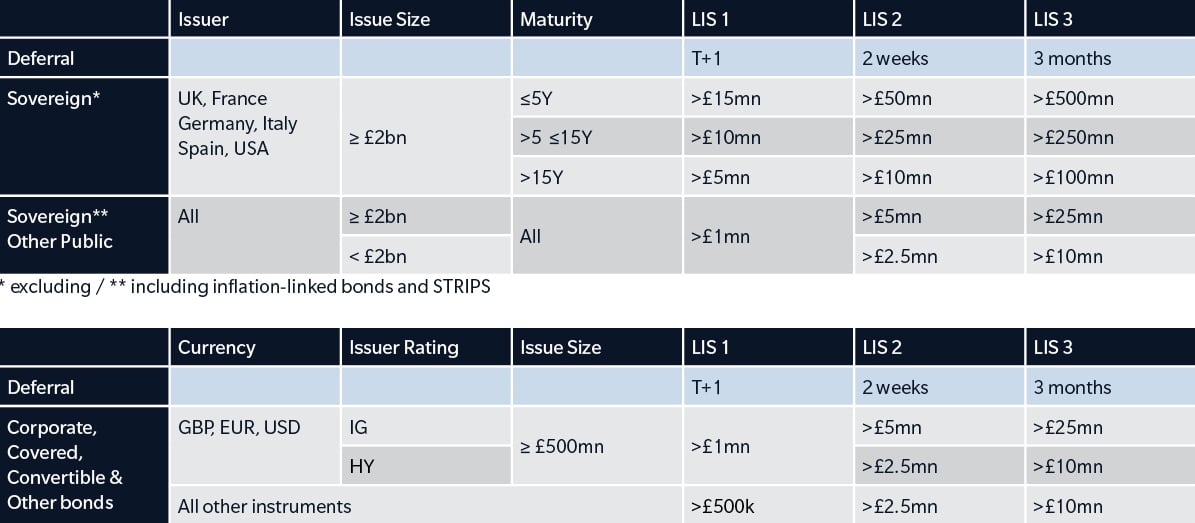

UK Transparency Financial Instrument Scope

UK Bond Transparency

Laying the groundwork for Consolidated Tapes

All changes follow the earlier removal of pre-trade transparency requirements for request-for-quote (RFQ) systems, further focusing attention on the post-trade element of reporting. With the new regime in effect, post-trade transparency has become the primary mechanism through which market participants in the UK can observe executed activity and assess reported transaction data as part of their pre-trade decisions making process.

Consequently, the planned introduction of Consolidated Tape Providers (CTPs) in both the UK and the EU is central to the transparency reforms. These are regulated entities that gather, combine, and distribute real-time (and deferred) trading data from various financial markets into a single output, enhancing market transparency and efficiency. The first wave will focus on bonds – potentially as early as June 2026 in the UK – followed by a tape for equities and ETFs, with the FCA yet to state its intention regarding derivatives. The EU sequence follows the same pattern, but the go-live of the EU bond CTP may trail that of the UK’s, while also including a clear intention for a derivatives CTP in the future.

It's all in the numbers

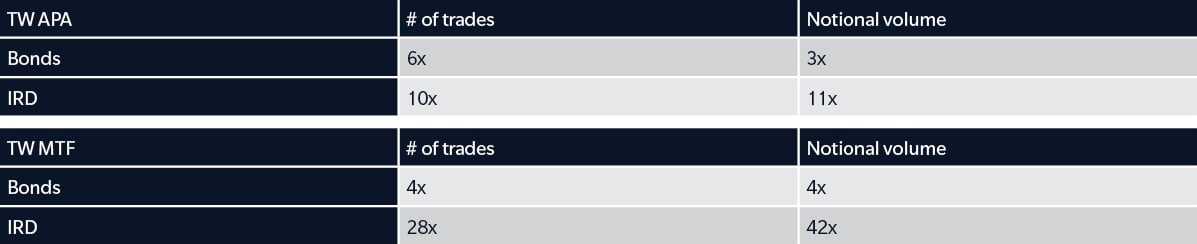

The shift in reported data during the first few days of implementation was immediate and significant. Tradeweb observed a substantial increase in the volume of real-time publications across both its UK Multilateral Trading Facility (MTF) and Approved Publication Arrangement (APA). Initial analysis indicates that real-time bond transparency was approximately five times higher than the daily averages recorded in the preceding week, with an even higher impact on interest rate derivatives. In line with expectations, this reflects the broadened scope of trades now subject to immediate publication, as well as the streamlined structure governing when information must be made public.

The below table indicates the factors by which real-time transparency publications improved during the week of December 1 in comparison to the week of November 24. Tradeweb observes an almost identical share of real-time reporting in sovereign bonds and slightly lower for corporate bonds, as modelled by the FCA.

What to expect from the EU’s transparency shift

An even more pronounced shift is expected when the EU’s revised transparency regime takes effect on March 2, 2026. Its changes apply to bonds, exchange-traded commodities and notes (ETCs & ETNs), and structured finance products (SFPs), with derivatives expected at a later stage. Whereas the UK model now centres on a single point of publication for price and volume, either in real time or at a defined deferral, the EU framework retains a multi-layered approach in which price and volume may be disseminated at different times.

The EU regime also applies a wider set of conditions to determine eligibility for real-time release and introduces a more granular sequence of deferrals. Transparency data will therefore follow separate and distinct publication patterns across the two jurisdictions that are inextricably linked, creating a differentiated landscape for firms that consume cross-border post-trade information. The early response to the UK changes suggests that market participants are increasingly likely to focus on how to aggregate, compare and interpret transparency data as these reforms progress.

Looking ahead

The transition to the new UK framework, combined with the forthcoming EU adjustments, is expected to prompt renewed consideration of data workflows and transparency consumption in the months ahead. Tradeweb will continue to track publication trends and share further updates as more data becomes available.

If you would like to explore the new UK post-trade transparency regime in more detail, you can visit our real-time MiFID publication site, where prints from our UK MTF and APA are available here - select “Contact us for real-time access” if you need login details. For any additional guidance on using MiFID post-trade data, your Tradeweb relationship manager can share those resources with you.